| Market sentiment – figures show a sharp deterioration in market sentiment as geopolitical tensions rise in the Middle East | BTR investment – figures highlight the resilience of residential rental markets as investors remain attracted to stable income streams | UK holiday let market – overall demand remains stable, despite travellers becoming increasingly selective |

Geopolitical uncertainty hits confidence

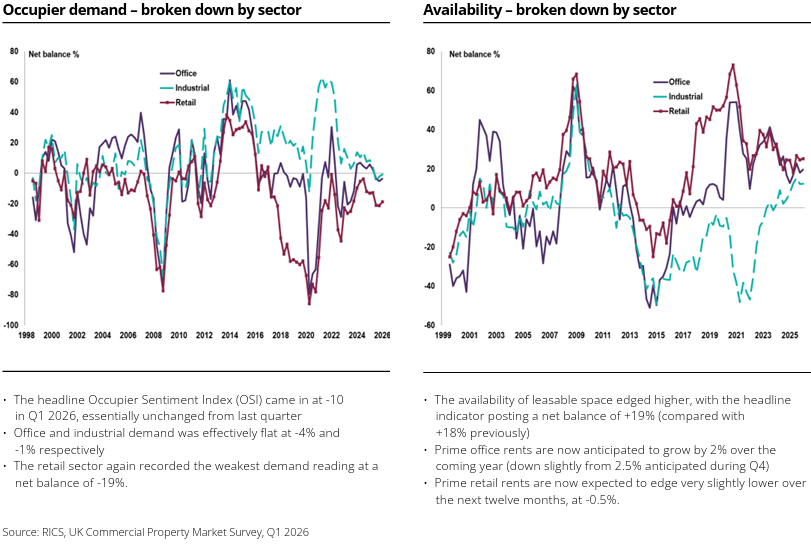

The Royal Institution of Chartered Surveyors (RICS) Commercial Property Monitor for Q1 2026 highlights a sharp deterioration in market sentiment as geopolitical tensions weigh on investor confidence.

Survey respondents pointed to rising energy costs, inflation concerns and higher bond yields as key pressures affect the sector. Most notably, the credit conditions indicator fell sharply to -44%, down from +9% in Q4 2025, marking the weakest reading since 2023.

While investment activity has softened and expectations for capital values have weakened, occupier demand has remained relatively stable. Prime office and industrial rents are still forecast to grow modestly over the next year, particularly in London, although projections have been revised down. Alternative sectors such as data centres, life sciences and aged care continue to outperform traditional markets.

Overall, the report suggests that commercial property recovery is losing momentum amid growing economic uncertainty and tighter financing conditions.

BTR investment holds strong

Investors committed around £679m to acquiring or funding Build-to-Rent (BTR) assets during Q1 2026, demonstrating continued confidence in the sector.

Knight Frank figures highlight the resilience of residential rental markets as investors remain attracted to stable long-term income streams and sustained tenant demand.

Although higher borrowing costs and geopolitical tensions have created more cautious conditions across the wider property market, BTR continues to benefit from structural undersupply in UK housing and strong rental growth. Institutional investors are particularly focused on high-quality schemes in major regional cities and London, where demand for professionally managed rental accommodation remains robust.

The sector’s appeal is also supported by changing lifestyle trends, affordability pressures in the sales market and the growing preference for flexible urban living. While transaction activity across commercial real estate has slowed, the strong level of BTR investment suggests it remains one of the most attractive areas of the UK property market.

Quality drives UK holiday let market

The UK holiday accommodation sector has remained resilient despite economic pressures, regulatory changes and evolving consumer habits, say Savills.

While overall demand remains stable, travellers are increasingly selective, with shorter stays, later bookings and higher expectations. Rather than compromise on quality, guests prioritise premium accommodation and experience-led breaks, helping high-quality operators maintain strong occupancy levels.

The report highlights changing trends, particularly among DINKYs (dual-income, no kids yet), who are driving demand for short breaks focused on wellness, dining and personalised experiences. Multigenerational travel is growing, with families seeking spacious accommodation and onsite amenities suited for all ages.

Operators also face rising regulatory and operational pressures, including changes to short-term let licensing and business rates. Looking ahead, the sector is expected to favour businesses that can combine high standards with flexible, experience-focused offerings while adapting to an increasingly complex operating environment.

Commercial Property Outlook

Demand in Scotland hit by global uncertainty

Commercial property demand in Scotland weakened in Q1 2026, according to the Royal Institution of Chartered Surveyors (RICS) Commercial Property Monitor.

Investor appetite fell overall, particularly in the office and retail sectors, while industrial demand showed only a slight increase. Occupier demand was largely flat, marking its first non-positive reading since late 2022.

The report highlights a growing divergence between sectors – industrial space continues to see demand growth, while retail demand has declined and office demand has stagnated. Looking ahead, survey respondents expect capital values to edge lower in the near term, reflecting caution driven by geopolitical tensions in the Middle East.

Despite weaker sentiment, rental expectations are slightly more optimistic. A net +10% of respondents anticipate rents will rise over the next three months, driven by growth in industrial and office sectors, although retail rents are expected to fall.

All details are correct at the time of writing (20 May 2026)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.